25 March 2026 · 7 min read

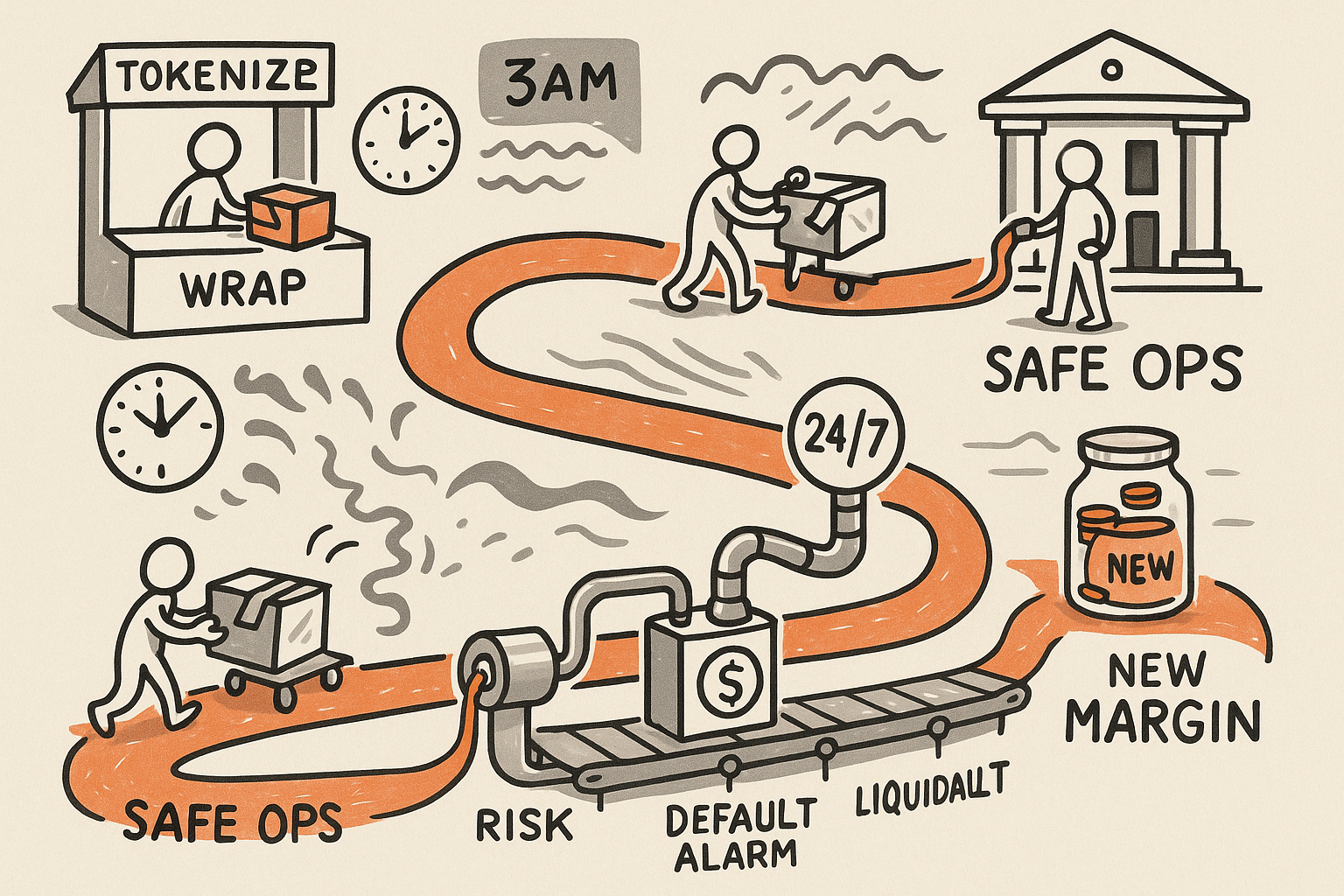

Tokenization Is the Wrapper. 24/7 Stablecoin Settlement Is the Rewrite.

When money moves instantly and always-on, the winners stop selling access and start shipping risk engines, controls, and recovery.

Most teams talk about tokenization like it is the wedge. Put the asset on-chain, add a prettier interface, compress a few intermediaries, and call it innovation.

I do not buy that framing.

The real rewrite happens when settlement becomes instant and 24/7, and the unit of account is a stable digital cash instrument that can move at any time, not just during market hours. That shift is not cosmetic. It changes what “safe” means, what “operationally ready” means, and who captures margin.

I have lived versions of this problem outside capital markets. When I ran an international business unit in smart-building and home-automation, the product was not only sensors and controls. The product was also uptime, monitoring, incident response, and the confidence that a building would behave correctly at 3am on a Sunday. In those environments, the commercial winners treat exception handling and recovery as first-class features, not as back-office glue.

24/7 settlement pushes financial infrastructure in the same direction. The firms that win will not be the ones that “tokenize instruments.” They will be the ones that ship risk engines, liquidation rails, and surveillance that institutions can plug into and trust when humans are asleep.

The moment settlement goes always-on, your operating model breaks

In a batch world, you can pretend risk is a daily ritual. You calculate exposures at set times. You call for margin on a schedule. You reconcile overnight. You have committees for exceptions. You have humans in the loop because the loop is slow enough to tolerate them.

Always-on settlement removes the buffering. It turns a market into a continuous system.

- Margining becomes continuous. Not “end of day,” not “intraday window,” but an always-evaluated requirement tied to live exposures and live collateral.

- Default management becomes a software loop. Detection, escalation, containment, and resolution have to run as code paths with clear timeouts, not as email threads.

- Liquidation becomes an execution product. If collateral can move instantly, liquidation is no longer a rare event handled by a specialist desk. It is a routine mechanism that must be designed, monitored, and optimized.

That forces a hard question for boards and operators: are you building a marketplace, or are you building a control plane?

Tokenization is the wrapper. Settlement is the control plane.

Brokerage economics move from distribution to “risk plus controls”

In a world where settlement is slow and the rails are scarce, distribution has real power. Whoever owns access, relationships, and account opening can charge tolls.

In a world where settlement is instant and programmable, distribution still matters, but it stops being defensible by default. What becomes defensible is the ability to keep the system safe under stress.

That sounds abstract until you translate it into what actually gets budget and headcount:

- Risk engines that compute exposure in real time and can explain it (to risk, to audit, to regulators) without storytelling.

- Controls that prevent bad states, not only detect them. Limits, circuit-breakers, concentration caps, velocity checks, and policy enforcement that can run unattended.

- Recovery as a designed capability. Roll forward, roll back, isolate, replay, and reconcile without freezing the whole business.

- Surveillance that is operational, not theatrical. Alerts tied to action playbooks, with measured false positives and measured response times.

This is why I keep coming back to manufacturing and industrial tech. When I spent years in power electronics and market quality, nobody argued that monitoring was “nice to have.” Monitoring was part of the product because it protected uptime, safety, warranty, and reputation. In financial infrastructure with 24/7 settlement, monitoring and recovery play the same role. They are not overhead. They are your moat.

If you want a parallel from my own venture work: building IBHQ forced me to think about broker operations as an everyday workflow problem, not a once-a-quarter governance problem. The tools that win are the ones that reduce exception volume and make the remaining exceptions resolvable fast, with a clear audit trail. Always-on settlement simply compresses the timelines and raises the stakes.

The product you are really shipping is “what happens when things go wrong”

In most board decks, the happy path gets 90 percent of the airtime. But in regulated, high-uptime systems, the happy path is table stakes. The product is the unhappy path.

I learned this the hard way as a former Head of R&D rebuilding a multi-discipline organization across embedded software, cloud, electronics, mechanics, and QA. Features were never the hard part. The hard part was building a machine that shipped reliably, caught regressions early, and recovered when something escaped. If you cannot do that in a thermostat or HVAC controller, you will not do it in a 24/7 settlement system where money is moving continuously.

So I use a simple operator lens: define the failure modes, then sell your ability to survive them.

Here are the failure modes that matter when settlement is instant and always-on:

- Latency and partial failure. Not “down” versus “up,” but degraded states. Can you keep clearing, or do you halt safely?

- Collateral quality drift. Not only price moves, but concentration and correlation surprises. Can you tighten policy automatically?

- Stuck transactions and reconciliation gaps. Can you reconcile continuously, or do you create an end-of-day cliff?

- Abuse and adversarial behavior. Always-on rails invite always-on exploitation. Can you detect and contain without punishing good flow?

- Human escalation at the worst possible time. Incidents happen at night and on weekends. Do you have runbooks, access control, and a practiced on-call muscle?

If this sounds like reliability engineering, it is. If it sounds like operations, it is. That is the point.

This is also why “tokenization strategy” is often the wrong conversation starter. The right starter is: what is our risk and controls product, and who is buying it?

A quarter-ready checklist: how to build for 24/7 settlement without fooling yourself

Boards and operators do not need more theory. They need moves they can fund, sequence, and govern. Here is the checklist I would use this quarter.

1) Choose your truth layer, and keep it boring

Decide what system is the financial source of truth. Define how balances, positions, collateral, and liabilities are represented. Lock the semantics. Avoid cleverness.

If you want to use AI, keep it out of the truth layer. Use it for narrative, triage, and operator assistance, not for determining balances. I have written about this more directly in LLMs in the narrative layer, not the financial truth layer.

2) Turn “margin” into a real-time service with explicit policies

Write margin as a service with versioned policies. Define triggers, grace periods, and automatic actions. Make every decision explainable. Treat policy changes like software releases with rollback.

3) Design liquidation as a product, not an emergency

Liquidation needs SLAs, observability, and controls. Define acceptable slippage, venues or routes, and anti-manipulation protections. Build kill switches and safe halts.

Put another way: liquidation is your last line of defense. Treat it with the same seriousness you treat payments.

4) Build an exception pipeline, not a ticket queue

Exceptions should flow through states with clear ownership and deadlines. Most organizations treat exceptions as unstructured work. That approach collapses under 24/7 settlement.

- Define top exception types and target volumes.

- Automate resolution for the top two.

- For the rest, build guided resolution with an audit trail.

5) Make reliability a commercial feature

Publish reliability commitments internally first: RTO, RPO, on-call response times, incident severity definitions. Then sell them. This is how you turn “ops cost” into “trust revenue.”

If your culture still treats ruggedization as paperwork, you will struggle. Reliability is a contract you pay for and enforce. I covered the same pattern in Ruggedization is a reliability contract.

My opinion: settlement is becoming the platform, and controls are the differentiator

Tokenization will keep expanding because it reduces friction in issuance and distribution. But tokenization alone does not decide the winners. Settlement does. Always-on settlement collapses time, and when time collapses, operations become product.

The next leaders in this space will look less like “tokenizers” and more like the best industrial operators I have worked with: obsessive about telemetry, disciplined about change control, and ruthless about closing the loop between detection and action.

If you are a board member or operator, here is the decision lens I would use: fund the control plane first. Fund the risk engine. Fund the liquidation rails. Fund surveillance and recovery. Make it work unattended. Then ship whatever wrappers you want on top.

Because in a 24/7 world, the question is not whether your product trades. The question is whether it keeps paying people correctly when everything is noisy.

When settlement is always-on, trust is no longer a brand promise. It is an operating system.

Newsletter

Working notes, straight to your inbox.

Occasional, no-noise notes on leadership, execution, and applied AI — from the field, not the sidelines.