1 April 2026 · 8 min read

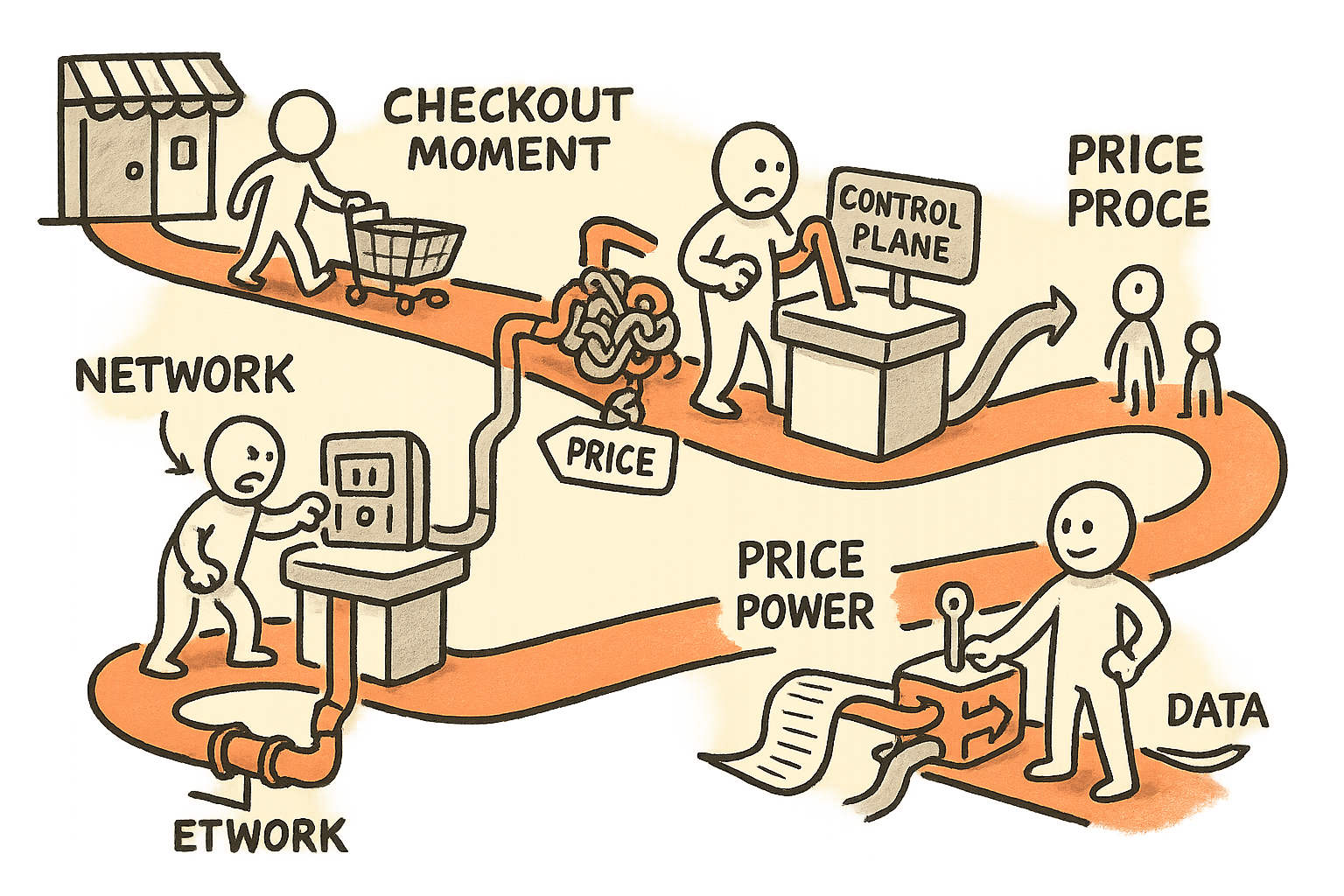

A Debit Network Is Not a Network. It Is the Checkout Control Plane.

If you treat payment rails like infrastructure, you miss the point. The asset is routing power, pricing leverage, and the right to harvest the data exhaust of every transaction.

I have never seen a durable profit pool that did not have a bottleneck attached to it. In manufacturing, it is a constrained line or a single qualified supplier. In industrial tech, it is a certification gate or a proprietary service tool. In software, it is a workflow users cannot leave without pain.

Payments looks like plumbing, but it behaves like control. A debit “network” is not primarily a set of pipes. It is the layer that influences routing decisions, pricing, acceptance, and the data exhaust that comes with every tap, swipe, and online checkout. Whoever owns that control plane owns the negotiation.

This is why I do not frame these assets as classic M&A logic. The strategic motive is upstream. It is about moving the bottleneck closer to the moment of purchase, where terms can be set before anyone else gets a fair chance to compete.

When I ran a P&L for a smart-building business unit, the pattern was the same: the product was not only sensors and controllers. The profit was in owning the interface that shaped specification, installation choices, and service workflows. Once we were specified and integrated, price discussions shifted. The customer’s alternatives became theoretical. Payments has the same physics. The checkout is the specification moment for money movement.

Control planes beat rails because they decide the defaults

Operators love throughput metrics because they are tangible. In payments, we talk about settlement speed, authorization rates, and uptime. Those matter. But they are table stakes. The game is won by whoever sets the default route, the default fee logic, and the default dispute behavior.

Think of a control plane as three levers:

- Routing power: who decides which path the transaction takes, and under what constraints.

- Pricing leverage: who can set or influence take rates, incentive structures, and volume tiers.

- Data exhaust: who captures the transaction metadata, and who can use it to improve risk, offers, underwriting, and retention.

If you control two of the three, you are hard to displace. If you control all three, you are the market.

In industrial automation, I spent eleven years around power electronics and market quality. The best analogy is not a better drive or a better converter. It is owning the commissioning toolchain and the service pathway. The plant may have many component suppliers, but the party that controls diagnostics and approved changes controls the long tail margin. Checkout routing is that toolchain.

Why this matters to merchants: “choice” exists until it is inconvenient

Merchants tend to assume they have routing optionality because, on paper, they can choose acquirers, gateways, and a stack of value-added services. In reality, optionality collapses when three things happen:

- Rules get bundled into a single commercial agreement, so “choice” requires renegotiating the entire stack.

- Operational friction rises, so switching costs are borne by store ops, finance, and customer support, not only by procurement.

- Performance is conditional, meaning the best auth rates, the best fraud tuning, or the fastest exception handling depends on staying inside one ecosystem.

I learned this the hard way in hospitality, when I co-founded and served as interim CEO of EatMore. We were building ordering and loyalty, and payments was always adjacent. The lesson was simple: merchants buy outcomes, not components. If the payment layer is packaged as “it just works,” it becomes the silent default. And defaults are where margin hides.

Board-level question for any merchant platform is not “What is our blended rate?” It is: Who can change our blended rate without asking us? If the answer is “someone upstream,” your negotiating position is weaker than your spreadsheet suggests.

Why this matters to fintechs: differentiation dies at the routing layer

Many fintech business models assume they can win by shaving bps, improving acceptance, or building a better user experience. All real. But if the pipes are effectively owned or steered by parties with different incentives, fintechs get trapped in three ways:

- Cost is capped: you cannot undercut a price you do not control. At best you get temporary promotions.

- Acceptance becomes permissioned: you are “accepted” as long as you do not threaten the control plane economics.

- Roadmaps become reactive: you ship around policy changes and routing constraints instead of building product advantage.

This is where I bring my venture-builder lens. With Shopeno, I am building a commerce platform with 0 percent cost and 0 percent commission for local shop owners. That forces discipline about where economics can and cannot live. If you remove take rate, you must win on operational leverage, financing structures, or services that merchants pull, not fees they tolerate. You cannot build that if your cost base is one policy update away from moving against you.

Same for IBHQ and DM Trading. In fintech, the surface product is often clean and modern. The real dependency is the underlying control plane: routing, risk, and settlement rules. If your differentiation depends on a rail you do not influence, you are not building a moat. You are building a feature.

Stablecoins and on-chain rails: the competition is insertion, not throughput

On-chain rails are often discussed as faster and cheaper. That discussion is incomplete. Even if a new rail is objectively better, it still has to be selected at the moment of checkout.

In other words, the hard part is not moving value. The hard part is getting into the routing decision loop where volume is steered. If incumbents control that loop, they can:

- keep new rails as an “edge case” option rather than a default,

- price-match selectively to remove urgency,

- restrict access via compliance, certification, or commercial packaging.

I saw a similar dynamic in connected building systems. Better sensors existed everywhere. The winners were the ones integrated into the specification, installer workflow, and facility maintenance loop. Once the workflow was owned, the technology debate stopped being neutral. It became a governance debate.

If you build on-chain payments, ask one question early: What is our insertion point into the merchant’s routing layer? If the answer is “a separate button,” you are already losing. If the answer is “a behind-the-scenes route chosen by policy,” now you are competing where it matters.

An operator’s checklist: defend or acquire the checkout control plane

Whether you are a bank, a merchant, or a fintech, you need a control-plane strategy. Not a partnership slide. A strategy with ownership, fallbacks, and measurable leverage.

1) Map the routing decision chain end to end

- Who decides the route today: POS, gateway, acquirer, issuer rules, network rules?

- Where can a third party override “your” preference?

- What are the constraints: uptime SLAs, tokenization, fraud tools, dispute handling?

If you cannot draw it, you cannot negotiate it.

2) Put the economics next to the control rights

- Which party earns based on volume, and which earns based on spread?

- Who benefits when routing consolidates?

- Who pays when exceptions spike (chargebacks, returns, manual reviews)?

The party that pays for exceptions will eventually demand control over routing. That is governance, not technology.

3) Treat data exhaust as a product, not a byproduct

- What transaction fields do you see, and what fields are masked?

- Do you have the right to use the data for underwriting, offers, or fraud?

- Can your model improve with scale, or is the learning captured upstream?

If you are building applied AI in payments, this is existential. If you do not own the data contract, you do not own the learning curve. If you want a parallel example of how I think about “contracts” that look like technical details but behave like economics, see eSIM as a trust anchor.

4) Build a credible failover that is commercial, not only technical

- Can you move volume in 30 days without breaking operations?

- Do you have pre-negotiated terms for the alternative path?

- Do you have monitoring that proves performance differences, not anecdotes?

In operations, I always insisted on a “Plan B that ships.” In electrification and energy storage, failover is physical. In payments, it is contractual and procedural. Both are real. This is also why I value an operator’s “stop button” mindset in automation, even outside AI contexts. The same thinking appears in AI value and the stop button.

5) Decide what you must own

- Merchants: own the routing policy logic, even if you outsource execution.

- Fintechs: own at least one lever (cost, acceptance, or data) directly, not via goodwill.

- Banks: if you want to set terms, own the interface where terms are chosen.

Ownership can be software, contracts, or governance. But it must be enforceable.

My opinion: stop calling it infrastructure and start calling it power

The checkout moment looks small. A card tap. A green checkmark. A receipt. But that moment is where routing is decided, pricing is embedded, and data is emitted. Whoever controls that layer does not need to win every product battle. They can simply set the rules of engagement.

If you are on a board, ask management for a control-plane memo, not a payment vendor update. If you run a merchant or fintech P&L, treat routing optionality like a strategic asset and fund it like insurance. And if you build new rails, aim for insertion into the routing layer, not a parallel experience that competes on ideals.

In every industry I have operated in, from factory systems to SaaS to fintech, the same law applies: the bottleneck sets the terms. Payments is no different. The control plane is the bottleneck.

Newsletter

Working notes, straight to your inbox.

Occasional, no-noise notes on leadership, execution, and applied AI — from the field, not the sidelines.