24 June 2026 · 9 min read

MiCA 2.0 Will Be Won in Ops Liability, Not Issuance Rules

If the customer cannot get an answer, a reversal, or a clear owner of loss, your token is just a new way to create old disputes.

I have a simple bias from running cross-border organizations: rules do not protect customers, operating systems do. The law can say “authorized to issue.” It can define reserves. It can define disclosure. None of that matters the moment a customer’s funds are stuck between an EU distributor, a non-EU issuer, a wallet provider, a bank, and a support inbox that does not answer.

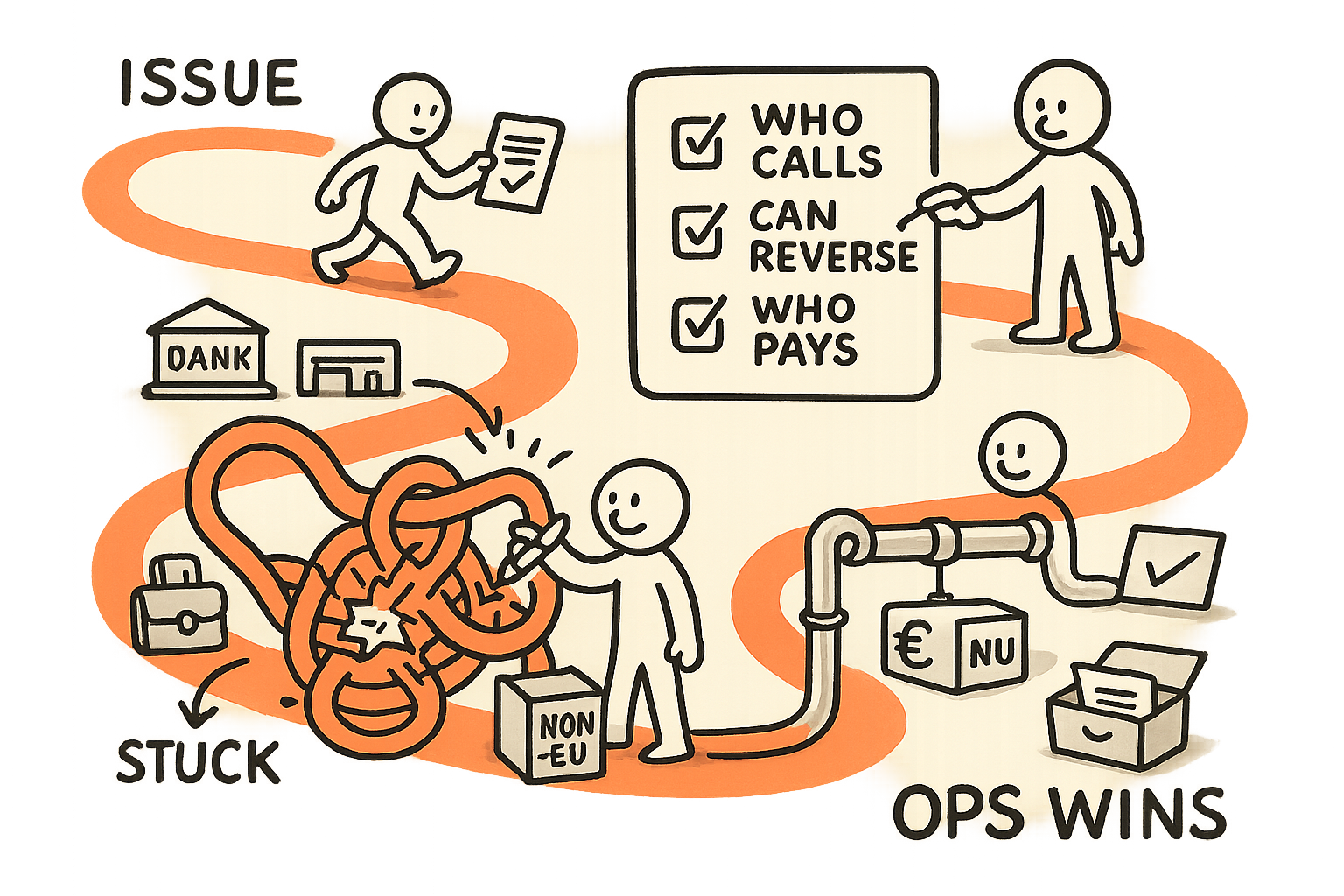

In that moment, the customer asks three questions. Who picks up the phone. Who can reverse. Who eats the loss.

That is why I believe the next iteration of European crypto regulation, call it MiCA 2.0 or anything else, will not be won in issuance rules. It will be won in ops liability and dispute plumbing. The hardest part is not “permission to issue.” The hard part is making responsibility explicit across the distribution stack, across jurisdictions, and across intermediaries that each have their own incentives.

When I ran a multi-country business unit in smart building and home automation, my life was not governed by product specs alone. It was governed by escalations. A sensor failing in the field did not care about our org chart. The customer wanted a clear owner, a timeline, and a fix. In payments and tokenized money, the “field failure” is a stuck transfer, a duplicate debit, a misrouted on-chain payout, or a sanctioned counterparty exposure discovered too late. The mechanics differ. The operational truth is the same.

The messy middle is the product

Most teams treat distribution and dispute handling as “after launch” work. That is a mistake. In regulated money movement, the messy middle is the product. It includes:

- Distribution controls: who is allowed to onboard, fund, redeem, and under what conditions.

- Customer support and complaints: intake, triage, timelines, and audit trails.

- Exception handling: what happens when a transfer is delayed, funds are frozen, or a counterparty is flagged.

- Dispute flows: chargeback-like reversals, partial refunds, misdirected payments, and double-spend equivalents in the real world.

- Loss allocation: who pays when an error is not recoverable.

The customer does not care whether the underlying rail is a stablecoin, a tokenized deposit, or a bank transfer. They care that their balance is correct and usable, that they can get help, and that someone can put the system back into a valid state when reality breaks your happy path.

This is also where most “innovations” quietly reintroduce risk. Tokenization often removes a familiar reversal mechanism and replaces it with “finality.” Finality is great for settlement. It is terrible for customer experience when you have fraud, fat-fingered addresses, compromised accounts, or merchant disputes. If your operating model cannot restore justice quickly, the regulator will, and it will do it in the most expensive way: by forcing liability onto whoever is easiest to supervise.

Regulation only becomes real when the SLA is explicit

I learned in industrial technology that governance without enforceable interfaces is theater. During my years in power electronics, quality issues were never solved by stating “we care about quality.” They were solved by defining the contract between engineering, production, suppliers, and service: what constitutes a defect, how it is reported, who owns containment, who owns root cause, and how quickly corrective actions must land.

Financial regulation is the same pattern, just with money instead of hardware. If you want to know whether a tokenized money scheme is robust, ask for the operational contract, not the whitepaper.

As an operator and board member, I would push for five explicit SLAs across the stack:

- Time to acknowledge: how fast a user complaint gets a human-confirmed ticket number, not an auto-reply.

- Time to freeze: how fast you can stop further harm when fraud is suspected. This is the “stop button” for payments.

- Time to reconcile: how fast you can prove what happened across ledger, bank accounts, and intermediaries.

- Time to provisional credit or denial: when the customer is made whole temporarily, or when you formally refuse with reasons.

- Time to final resolution: closure with full audit trail and loss allocation.

If you cannot write these down and attach an owner to each, you do not have a compliant system. You have a demo.

This is also why I often tell fintech teams to study industrial incident response. In a plant, you do not “wait and see” when temperature goes out of range. You stop the line, isolate the problem, and only restart when you can prove stability. Money movement deserves the same discipline. I wrote about this mental model in AI Value Isn’t in the Org Chart. It’s in the Stop Button. The principle is identical: authority to stop is part of governance.

Ops liability: decide it early, or it will be decided for you

In cross-border setups, the default outcome is predictable. Risk gets pushed downhill to the weakest link. The distributor says “issuer problem.” The issuer says “wallet problem.” The wallet says “user error.” The customer says “not my problem.” The regulator says “everyone is responsible,” and then picks the entity it can fine.

To avoid that, you need a liability model that is designed, not implied.

I like to frame it as a simple RACI plus balance sheet reality:

- Responsible: who runs the process day to day (the team that actually moves the levers).

- Accountable: who signs the policy and is on the hook when it fails (one entity, not a committee).

- Consulted: who provides input (compliance, banking partners, chain analytics, fraud vendors).

- Informed: who needs visibility (board, regulators, key distribution partners).

Then add the two questions most teams avoid:

- Who has the authority to reverse or compensate when the rail does not support reversal?

- Where is the loss absorbed when recovery is impossible, and how is that reserve funded?

If you are building stablecoin or tokenized money distribution, you are effectively building a consumer protection layer. You can pretend you are not, but you will still end up doing the work when disputes hit scale.

In my own venture building, I treat this as design input, not compliance overhead. With IBHQ, where workflows touch onboarding, risk checks, and partner operations, I am allergic to “someone else will handle it” thinking. The moment you scale, “someone else” becomes “nobody,” and you get a backlog of exceptions that destroys trust.

The dispute control plane: build it like a real system

Dispute plumbing sounds boring until you quantify its impact. It affects conversion, retention, support cost, fraud loss, and regulatory risk. It is also the place where most tokenized schemes are weakest, because the underlying rails were not built for consumer disputes.

So build a dispute control plane explicitly. Practically, that means:

1) A shared event model across parties

If your distributor, issuer, and wallet provider each have different transaction identifiers, you will never reconcile at speed. You need a shared reference model that links: user, funding source, on-chain tx, off-chain ledger entries, fees, and settlement state.

This is similar to what I saw in manufacturing and connected devices: if service tickets cannot be tied to a specific hardware revision, firmware version, and batch, you do not have traceability. Payments are no different. Traceability is the foundation of resolution.

2) A clear escalation path that crosses company boundaries

When an incident crosses jurisdictions, the escalation must still be one hop. Not five emails and a weekly call. Define the escalation ladder, the on-call structure, and the decision rights. If it is not tested, it does not exist.

3) Pre-defined dispute types and playbooks

Do not treat every case as bespoke. Create a taxonomy: unauthorized transfer, duplicate debit, wrong recipient, merchant dispute, sanctions-related freeze, technical outage, KYC mismatch, and so on. Each type gets a playbook, a data checklist, and a target resolution time.

4) A “reversal equivalent” mechanism

On-chain finality does not remove the need for reversals. It just changes how you implement them. You need a policy and a mechanism for customer restitution: internal ledger adjustments, reserve-funded credits, clawback where legally and technically possible, and explicit eligibility criteria.

This is where many teams confuse technical architecture with operating architecture. The operating architecture is what regulators and customers will feel.

5) A measurable error budget

In industrial operations, you manage reliability with error budgets and containment. Apply the same discipline to disputes. Decide acceptable thresholds for failed settlements, reconciliation breaks, support response times, and fraud loss. Then staff and automate to stay within those thresholds.

This connects to how I think about control planes in payments. The rail is not the product. The control plane is. If this resonates, A Debit Network Is Not a Network. It Is the Checkout Control Plane. unpacks the same idea from a different angle.

What I would ask for in the boardroom this quarter

If you are a board member or operator overseeing tokenized money or stablecoin distribution into Europe, do not start with the issuance license. Start with operability.

- Show me the dispute map: all parties, all handoffs, and where funds can get stuck.

- Show me the liability table: for each failure mode, who pays, who decides, and what evidence is required.

- Show me the SLAs: acknowledge, freeze, reconcile, provisional credit, final resolution.

- Show me the stop button: who can pause onboarding, pause redemptions, or halt a distribution channel, and under what criteria.

- Show me the reconciliation truth: one canonical ledger, and how it ties to bank accounts and on-chain transactions.

- Show me how you train partners: because your weakest link will be a third party with a script and no context.

If the answers are vague, the strategy is not “early.” It is unfinished.

When I built and ran EatMore, a hospitality ordering and loyalty platform, we won or lost on execution details that nobody put on the homepage: refunds, charge disputes, missing orders, and the ability to resolve issues fast across merchants and users. That experience made me stubborn about operational ownership. In regulated tokenized money, that stubbornness is not optional. It is the business.

The market will reward the token that feels boring in operations: predictable, reachable, reversible when it must be, and explicit about who carries the can.

My view is clear. If MiCA evolves to cover more instruments and more issuer footprints, the winners will not be the teams that can draft the cleanest issuance memo. They will be the teams that can prove, end to end, that disputes resolve inside a defined timeline, with a defined owner, and a defined loss model. That is what trust looks like in practice.

Everything else is just moving risk around the stack until it lands on the customer.

Newsletter

Working notes, straight to your inbox.

Occasional, no-noise notes on leadership, execution, and applied AI — from the field, not the sidelines.