25 February 2026 · 7 min read

An “HFT Layer-1” Is Not Faster Crypto. It Is a New Exchange Rulebook.

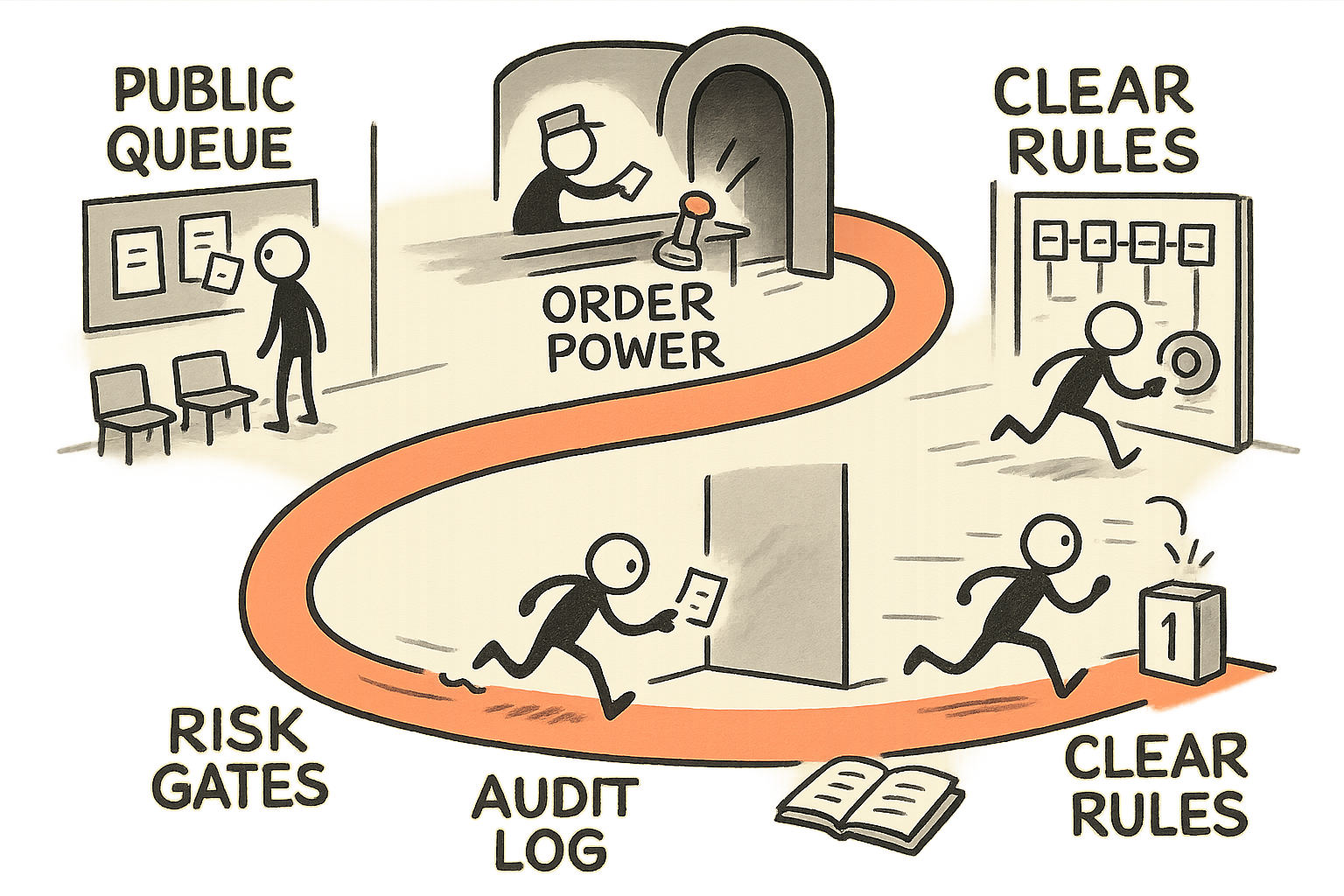

Remove the public queue and you do not eliminate friction. You privatize it, then you have to govern it like a market.

Every few years, someone tries to “make markets faster” by changing the plumbing. The pitch is always technical. Lower latency. Higher throughput. Fewer hops. Better UX.

But the moment you remove the public queue, you are not just speeding up a blockchain. You are writing a new exchange rulebook.

In practical terms, the public mempool is a messy, imperfect form of transparency. Everyone can see the waiting room. They can infer what might happen next. Once you replace that with streamed transactions and preconfirmation, you move ordering power upstream into the hands of whoever controls admission and sequencing. That party becomes a de facto matching layer, whether they call themselves a validator, a sequencer, a builder, or something else.

I have built and operated systems where speed mattered, including my own trading systems work with indicators and automation. I have also run organizations where reliability mattered more than elegance, like when I ran operations across engineering, production, and supply chain in electrification and energy storage. The lesson is the same: speed is cheap, trust is expensive. When you compress time, you amplify mistakes. When you privatize ordering, you create a new place to extract rent unless you design for auditability and fair allocation from day one.

This essay is a timeless operator’s lens on “HFT Layer-1” designs. Not as crypto theater. As market structure.

The technical change that becomes a governance change

A public mempool is a public queue. It is noisy and gameable, but it is legible. Participants can monitor it, build strategies around it, and at least argue about fairness with shared data.

Remove it, and you create an information asymmetry by design. Now there is a private intake. There is preconfirmation, which is essentially a promise about future ordering. There is streamed flow, which is essentially a privileged feed.

At that point, the core product is no longer “blockspace.” The product is:

- Ordering policy: who gets in first, and under which rules.

- Allocation: how priority is sold, earned, or distributed.

- Dispute handling: what happens when preconfirmation conflicts with final inclusion.

- Accountability: who can prove what happened, after the fact, with evidence.

That is why these designs should be evaluated like an exchange launch, not like a benchmark chart.

When ordering is private, MEV becomes “the business model”

Operators like to pretend MEV is a bug. In private ordering systems, it is often the business model, just not always named.

If one party controls ordering and can commit to preconfirmation, they control the difference between “I saw the flow first” and “I reacted first.” That difference is the spread. It might show up as explicit fees, implicit slippage, or opaque priority pricing. Either way, someone collects it.

There are only three sustainable outcomes:

- You accept rent collection and treat it as the cost of execution quality, like paying for a venue. Fine, but then you must regulate it internally with rules, audits, and enforcement.

- You commoditize ordering through transparent auctions and verifiable fairness. Hard, but possible if you make the allocation mechanism legible and auditable.

- You pretend it is decentralized while centralizing the power. That is the unstable path. It ends with reputation loss, regulatory heat, and sophisticated participants leaving.

In board terms, the question is not “Is it fast?” The question is “Who owns ordering, and what prevents them from taxing everyone else?”

Faster markets require broker-grade controls, not more TPS

Once you engineer away the public waiting room, you inherit a different set of hard problems. They are the same problems every serious venue, broker, or clearing-adjacent system deals with:

- Pre-trade risk limits: not after the trade. Before it. Max order size, max notional, max message rate, max open exposure.

- Credit throttles: what happens when an agent is acting on delegated capital. You need dynamic credit lines, not static balances.

- Kill switches: per account, per strategy, per API key, and venue-wide. Not “pause the chain.” A precise stop button. I wrote about this design pattern in AI value and the stop button, and it applies here too.

- Surveillance: manipulation detection, abusive quoting patterns, wash behavior, cross-venue games. If you cannot detect it, you are subsidizing it.

- Incident playbooks: when preconfirmations fail, when clocks drift, when a sequencer misbehaves, when network partitions happen. “We will fix it” is not a plan.

When I built IBHQ, a SaaS platform for Introducing-Broker businesses, the recurring theme was control planes. Brokers live and die by risk gates, not by pretty UIs. The venue can be fast, but if you cannot enforce limits at admission time, you eventually hand the keys to the most aggressive flow. Then everyone else pays for it through blowups, clawbacks, or hidden costs.

Speed without gates is not innovation. It is leverage.

A simple decision lens: who is the referee, and can we audit the game?

If you are a board member, owner, or operator evaluating a private-ordering L1 design, I would push the discussion into five concrete questions. You can use them this quarter, whether you are building the venue, integrating with it, or allocating capital to it.

1) What is the ordering policy, in plain language?

If the answer needs a whitepaper to decode, you have a governance problem. Ordering rules must be explainable to a risk committee in five minutes.

2) How is priority allocated, and is it verifiable?

Is it first-come-first-served based on receipt time. Is it auctioned. Is it relationship-based via a private stream. Whatever it is, you want two properties: predictability and auditability.

3) What is the dispute model between preconfirmation and finality?

Preconfirmation is a promise. Promises need remedies. What happens when the promise is broken. Who pays. How is evidence produced. If the only remedy is “social consensus,” you are running a club, not a market.

4) Where do risk gates live, and who controls them?

Venue-level gates should be built-in and enforced at the edge. Participant-level gates should be configurable and provable. If all gates are external, you will get systemic events. If all gates are internal and opaque, you will get trust decay.

5) How do you measure execution quality without self-reporting?

You need independent metrics. Not just TPS. Think in terms of slippage distributions, inclusion predictability, cancellation effectiveness, and tail behavior under stress.

This is the same mindset I used in industrial contexts. In power electronics, you can hit a lab spec and still fail in the field if you do not control variance, stress cases, and error budgets. Reliability is a contract you enforce, not a feature you claim. I made that argument directly in Ruggedization is a reliability contract. Markets are no different.

The uncomfortable truth: participants will accept centralization if the rules are clean

Many builders assume users only care about decentralization as a principle. In practice, serious participants care about:

- Fill quality.

- Predictable rules.

- Low dispute risk.

- Clear recourse when things break.

They will accept a more centralized ordering layer if it buys them those outcomes, especially when their alternative is a noisy public queue where they get picked off.

But this only works if the venue treats ordering and preconfirmation as regulated surfaces, even when no regulator is forcing the issue. In other words, you must govern yourself like an exchange because you are functionally becoming one.

That means transparent policies, audit logs, surveillance, and real consequences for abuse. It also means admitting a truth many teams avoid: if you want “institutional” flow, you are going to ship broker-grade controls and you are going to say no to some participants.

My opinion: design the rulebook first, then ship the speed

An “HFT Layer-1” is not a performance upgrade. It is a market redesign. The winners will not be the teams with the best latency story. They will be the teams that can answer, in operational terms, who controls ordering, how rents are constrained, and how failures are handled.

If you are building one, do not lead with throughput. Lead with governance: ordering policy, auditable allocation, dispute mechanisms, and risk gates that work under stress.

If you are integrating with one, do not start with connectivity. Start with execution quality measurement, limit frameworks, and a kill switch that you can trigger in one action.

Speed is easy to buy. Trust is expensive to earn. Private ordering systems can be worth it, but only if the rulebook is explicit, enforceable, and auditable.

Newsletter

Working notes, straight to your inbox.

Occasional, no-noise notes on leadership, execution, and applied AI — from the field, not the sidelines.